The global industrial landscape is witnessing a paradigm shift toward stricter environmental compliance and sustainable manufacturing practices. Coal based activated carbon, a highly porous form of carbon processed from bituminous, sub-bituminous, or lignite coal, has emerged as an indispensable material for purification, decolorization, and detoxification processes. From municipal water treatment plants removing trace contaminants to gold mining operations recovering precious metals, the versatility of coal based activated carbon underpins its widespread adoption. As we approach 2026, the market is poised for significant transformation driven by regulatory mandates, technological advancements in activation methods, and growing demand from emerging economies.

The coal based activated carbon market was valued at approximately USD 3.9 billion in 2023 and is projected to reach USD 5.2 billion by 2026, registering a compound annual growth rate (CAGR) of 5.8% during the forecast period 2024-2026. This growth is primarily attributed to rising investments in water and wastewater treatment infrastructure, stringent mercury and air toxic emission standards for coal fired power plants, and expanding applications in food and beverage processing, pharmaceutical purification, and automotive cabin air filters.

This comprehensive article analyzes the coal based activated carbon market through the lens of 2026, providing industry professionals, procurement specialists, and environmental compliance officers with data driven insights. We examine current trends, key growth drivers, regional dynamics, technological innovations, and emerging opportunities. The article also addresses competitive strategies, supply chain considerations, and potential challenges. All market data and forecasts are supported by reputable industry sources and research publications.

- Market Overview and Product Classification of Coal Based Activated Carbon

- Key Trends Shaping the Coal Based Activated Carbon Market

- Major Growth Drivers Leading to 2026

- Technological Innovations and Product Development

- Regional Market Analysis: Asia Pacific, North America, Europe, Middle East and Africa, and Latin America

- Future Opportunities and Strategic Recommendations for 2026 and Beyond

Market Overview and Product Classification of Coal Based Activated Carbon

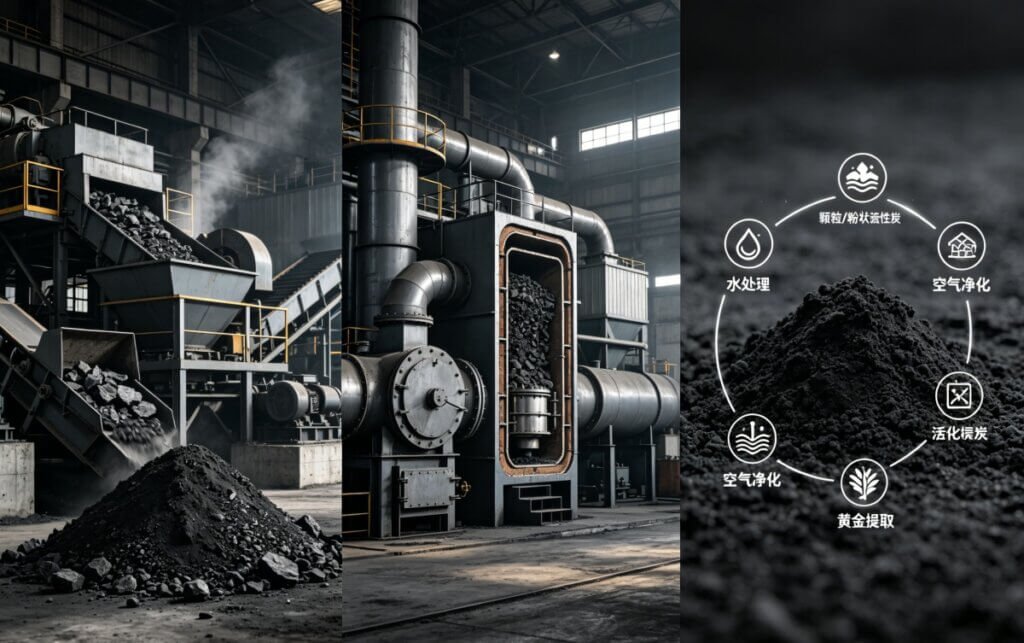

Coal based activated carbon is manufactured through thermal or chemical activation of coal feedstocks, producing a carbonaceous material with extensive microporous structure and high specific surface area ranging from 800 to 1500 m²/g. Depending on the activation method and coal type, the product is classified into powder activated carbon (PAC), granular activated carbon (GAC), and extruded or pelletized activated carbon (EAC), each serving distinct industrial applications.

Powder activated carbon consists of fine particles (typically less than 0.18 mm) and is widely used for liquid phase adsorption in batch processes such as municipal drinking water treatment, decolorization of sugar and edible oils, and pharmaceutical intermediate purification. Granular activated carbon features larger particle sizes (0.2 to 5 mm) and is preferred for continuous flow systems including industrial wastewater treatment, air purification, and solvent recovery. Extruded activated carbon, formed into cylindrical pellets, offers high mechanical strength and low pressure drop, making it ideal for gas phase applications like flue gas treatment, mercury removal from coal fired power plant emissions, and vapor adsorption systems.

The choice of coal feedstock significantly influences product properties. Bituminous coal based activated carbons exhibit high hardness and well developed microporosity, suitable for demanding gas phase applications. Lignite or sub-bituminous based carbons offer larger mesopore volumes and faster adsorption kinetics for liquid phase applications involving high molecular weight contaminants. According to industry technical data, the global distribution of coal based activated carbon production by type in 2023 shows granular activated carbon accounting for approximately 45% of market share, powder activated carbon 35%, and extruded activated carbon 20% (Source: Market Research Future, 2024).

Key Trends Shaping the Coal Based Activated Carbon Market

Four dominant trends are reshaping the coal based activated carbon market through 2026: the shift towards reactivation and circular economy models, increasing demand for tailored pore size distributions, integration of activated carbon with advanced oxidation processes, and the rise of smart monitoring systems for adsorption bed saturation detection.

Trend 1: Reactivation and circular economy. Rising raw material costs and environmental concerns are driving end users to invest in on site or third party reactivation services. Thermal reactivation regenerates spent activated carbon, restoring 85% to 95% of its original adsorption capacity. Major water utilities and industrial facilities now incorporate reactivation cycles into their procurement contracts, reducing total cost of ownership and landfill waste. The global activated carbon reactivation market is expected to grow at a CAGR of 6.2% from 2024 to 2026, outpacing virgin carbon growth rates.

Trend 2: Tailored pore size engineering. Conventional activated carbon products offer broad adsorption capabilities, but emerging applications require precise pore size distributions. For example, removal of microplastics and pharmaceutical residues from wastewater demands mesopores (2-50 nm), while gas phase mercury capture requires micropores (<2 nm). Manufacturers are investing in controlled activation processes using steam, carbon dioxide, or chemical agents (e.g., potassium hydroxide) to engineer pore architectures for specific contaminant profiles. This trend enables higher adsorption efficiency and longer service life.

Trend 3: Integration with advanced oxidation processes. Water treatment plants increasingly combine activated carbon with ozone, hydrogen peroxide, or ultraviolet light to achieve complete mineralization of refractory organic compounds. Coal based activated carbon serves as both an adsorbent and a catalyst support, enhancing the degradation of per and polyfluoroalkyl substances (PFAS), pesticides, and industrial solvents. This hybrid approach is gaining traction in regions with stringent discharge limits for emerging contaminants.

Trend 4: Smart saturation monitoring. Real time monitoring of activated carbon bed saturation using conductivity probes, ultraviolet absorbance sensors, or fluorescent tracers allows predictive maintenance and optimized carbon replacement schedules. Digital solutions integrated with supervisory control and data acquisition (SCADA) systems reduce operational costs by 15% to 25% while preventing breakthrough events. Adoption is accelerating in large scale municipal water plants and industrial wastewater facilities.

Major Growth Drivers Leading to 2026

The coal based activated carbon market is propelled by five primary growth drivers: stringent environmental regulations for mercury and air toxics, expansion of municipal and industrial wastewater treatment capacity, rising demand from gold mining for carbon in pulp and carbon in leach processes, increasing consumption in food and beverage purification, and the rapid industrialization of Southeast Asian and African economies.

Driver 1: Mercury and air toxic emission standards. The U.S. Environmental Protection Agency Mercury and Air Toxics Standards (MATS) and similar regulations in China (Ultra Low Emission standards) require coal fired power plants and industrial boilers to reduce mercury emissions by over 90%. Activated carbon injection (ACI) technology, using powdered coal based activated carbon, remains the most cost effective compliance method. Approximately 65% of U.S. coal fired power plants currently employ ACI systems, and China is mandating full compliance by the end of 2025. This regulatory push alone accounts for an estimated 8% annual growth in coal based PAC demand.

Driver 2: Water and wastewater treatment expansion. The United Nations estimates that global water demand will exceed supply by 40% by 2030, prompting massive investments in water reuse and advanced treatment. Coal based activated carbon is essential for removing disinfection byproduct precursors, taste and odor compounds (geosmin and 2-methylisoborneol), perchlorate, and trace organic contaminants. China’s 14th Five Year Plan allocates USD 80 billion for water environment improvement, including new activated carbon filtration at thousands of municipal plants. India’s Namami Gange program and the European Union Urban Wastewater Treatment Directive revisions further drive demand.

Driver 3: Gold mining recovery processes. The carbon in pulp (CIP) and carbon in leach (CIL) processes, which use granular activated carbon to adsorb gold cyanide complexes, account for over 70% of global gold production. With gold prices remaining above USD 1,800 per ounce and new mining projects opening in West Africa, Canada, and Australia, the demand for high hardness, high activity coal based activated carbon is rising. Mining grade activated carbon requires exceptional abrasion resistance (less than 1% attrition loss) to minimize gold losses and carbon consumption.

Driver 4: Food and beverage purification. Strict food safety standards, including the U.S. Food Safety Modernization Act and European Commission regulations on contaminant levels, require activated carbon treatment for edible oils, sweeteners, alcoholic beverages, and fruit juices. Coal based activated carbon is preferred for its consistent quality, low ash content, and high decolorization efficiency. The global plant based beverage market, growing at 11% annually, further increases demand for activated carbon to remove off flavors and undesirable compounds.

Driver 5: Industrialization in emerging economies. Vietnam, Indonesia, Nigeria, and Kenya are rapidly expanding their manufacturing bases, leading to higher industrial emissions and wastewater volumes. Local environmental agencies are adopting regulations modeled on EU and U.S. standards, creating new markets for coal based activated carbon. Domestic production capacity in these countries remains limited, driving imports from major producers such as China, India, and the United States.

Technological Innovations and Product Development

Recent technological breakthroughs in coal based activated carbon manufacturing include chemical activation using potassium hydroxide to achieve ultra high surface areas exceeding 2,500 m²/g, impregnation with sulfur or halogens for enhanced mercury and hydrogen sulfide removal, and development of magnetically recoverable activated carbon composites for simplified separation in slurry phase applications.

Ultra high surface area carbons. Traditional steam activated carbons typically achieve surface areas of 800 to 1,200 m²/g. Potassium hydroxide (KOH) activation, operated at 700 to 900°C, creates extensive microporosity with surface areas up to 3,000 m²/g. These materials demonstrate exceptional capacity for methane and hydrogen storage, supercapacitor electrodes, and adsorption of large organic molecules. Although production costs are higher, niche applications in energy storage and specialty chemical purification are driving commercialization. Several Asian manufacturers have launched KOH activated coal based products priced 40% above conventional grades but offering triple the adsorption capacity for certain compounds.

Impregnated activated carbons. To target specific inorganic pollutants, manufacturers impregnate coal based activated carbon with chemical additives. Sulfur impregnation (5-15% by weight) enhances mercury capture in flue gas by forming stable mercuric sulfide. Bromine or iodine impregnation improves mercury oxidation and retention, particularly for low rank coals with high halogen content. Caustic or potassium carbonate impregnated carbons are effective for hydrogen sulfide and acid gas removal in biogas upgrading and sewage treatment plant odor control. The global impregnated activated carbon market segment is forecast to grow at 7.2% CAGR through 2026.

Magnetically recoverable composites. In batch treatment processes where powder activated carbon is dispersed into liquids, recovering the spent carbon from treated effluent is challenging and costly. Researchers have developed composite particles combining coal based activated carbon with iron oxide nanoparticles. These magnetic activated carbons can be rapidly separated using low intensity magnetic fields, enabling multiple reuse cycles and eliminating filtration steps. Pilot scale studies demonstrate 95% recovery efficiency and retention of 85% adsorption capacity after five cycles. Commercial products are expected by late 2025, targeting pharmaceutical and fine chemical industries.

Comparison of coal based activated carbon types and their applications:

| Product Type | Particle Size | Typical Surface Area (m²/g) | Primary Applications |

|---|---|---|---|

| Powder Activated Carbon (PAC) | < 0.18 mm | 800 – 1,200 | Municipal water treatment, decolorization, pharmaceutical purification, mercury injection |

| Granular Activated Carbon (GAC) | 0.2 – 5 mm | 900 – 1,100 | Wastewater filters, air purification, solvent recovery, gold CIP/CIL |

| Extruded Activated Carbon (EAC) | 1 – 5 mm diameter, 3-15 mm length | 850 – 1,050 | Flue gas treatment, vapor recovery, catalytic supports, gas masks |

| KOH Activated Ultra High Surface Area | Varies | 2,000 – 3,000 | Supercapacitors, methane storage, high value chemical purification |

Source: Adapted from International Activated Carbon Conference Proceedings, 2024.

Regional Market Analysis: Asia Pacific, North America, Europe, Middle East and Africa, and Latin America

Asia Pacific dominates the coal based activated carbon market with over 50% share in 2023, driven by China’s massive production capacity and India’s rapidly growing water treatment sector. North America remains a key market due to strict mercury emission rules, while Europe leads in reactivation and circular economy adoption. The Middle East and Africa present the fastest growth opportunity, fueled by desalination pretreatment and gold mining expansion.

Asia Pacific (China, India, Japan, Southeast Asia). China accounts for nearly 70% of global coal based activated carbon production, with major manufacturing clusters in Shanxi, Ningxia, and Inner Mongolia. However, domestic environmental crackdowns on outdated production facilities are consolidating the industry, favoring larger, cleaner plants. India’s water and wastewater treatment market is expanding at 12% annually, with the National Mission for Clean Ganga requiring activated carbon systems at over 100 sewage treatment plants by 2026. Southeast Asian countries, particularly Vietnam and Indonesia, are implementing new industrial emission standards, creating import demand. Projected regional CAGR: 6.5% (2024-2026).

North America (United States, Canada, Mexico). The U.S. remains the largest consumer of coal based activated carbon for mercury control, with the MATS rule recently upheld by courts, ensuring continued demand through 2026. Additionally, the Bipartisan Infrastructure Law allocates USD 55 billion for drinking water and wastewater infrastructure upgrades, including lead and PFAS removal using granular activated carbon. Canada’s strengthened Mining Effluent Regulations and Mexico’s industrial wastewater discharge limits further support market growth. Projected regional CAGR: 4.2%.

Europe (Germany, France, UK, Italy, Benelux, Nordic countries). Europe leads in activated carbon reactivation, with over 35% of used carbon being thermally regenerated compared to less than 15% globally. Stringent Industrial Emissions Directive (IED) and Urban Wastewater Treatment Directive revisions require advanced treatment for micropollutants. Germany’s fourth regulatory framework for trace substances and France’s plan to equip all major water treatment plants with activated carbon filtration by 2026 drive demand. However, a shift toward bio based and coconut shell activated carbon in some consumer facing applications limits coal based growth. Projected regional CAGR: 3.8%.

Middle East and Africa (Saudi Arabia, UAE, South Africa, Ghana, Senegal). Desalination plants in the Gulf region use granular activated carbon as pretreatment to remove chlorine, organic matter, and taste causing compounds before reverse osmosis. South Africa’s aging water infrastructure and industrial pollution create replacement demand. West African gold mining (Ghana, Burkina Faso, Senegal) is booming, with new CIP/CIL facilities requiring high quality coal based activated carbon. Limited local manufacturing means most product is imported from China, India, and the U.S. Projected regional CAGR: 7.2% (fastest globally).

Latin America (Brazil, Mexico, Chile, Argentina). Brazil’s new regulatory framework for sanitation (Marco Legal do Saneamento) aims to achieve 99% water coverage by 2033, driving activated carbon purchases. Chile’s mining industry, including copper and lithium operations, uses activated carbon for water recovery and purification. Argentina’s oil and gas sector requires activated carbon for mercury removal from natural gas. Projected regional CAGR: 5.5%.

Future Opportunities and Strategic Recommendations for 2026 and Beyond

Three major opportunities will define the coal based activated carbon market beyond 2026: development of PFAS specific adsorbents, integration of activated carbon with biological treatment systems, and expansion into indoor air quality and electric vehicle cabin air filtration. Strategic recommendations include investing in reactivation infrastructure, diversifying feedstock procurement, and forming long term supply agreements with municipal and industrial clients.

Opportunity 1: PFAS specific adsorbents. Per and polyfluoroalkyl substances (PFAS), known as forever chemicals, contaminate drinking water sources worldwide. The U.S. Environmental Protection Agency has proposed maximum contaminant levels of 4 parts per trillion for PFOA and PFOS, which will require advanced treatment at thousands of water utilities. Standard activated carbon has limited capacity for short chain PFAS. Coal based activated carbon modified with cationic polymers, quaternary ammonium compounds, or carbon nanotubes shows enhanced PFAS removal. Manufacturers who develop PFAS tailored products will capture premium pricing and long term municipal contracts. The global PFAS remediation market is projected to reach USD 5 billion by 2026, with activated carbon representing a major share.

Opportunity 2: Integration with biological treatment. Biologically active carbon (BAC) filters combine adsorption with microbial degradation, extending carbon service life and reducing replacement frequency. In BAC systems, granular activated carbon supports a biofilm that metabolizes adsorbed organic compounds, continuously regenerating adsorption sites. This technology is gaining acceptance in drinking water treatment for removing natural organic matter and in industrial wastewater for trace organics. Coal based activated carbon with rough surfaces and high internal porosity promotes biofilm formation. Water utilities adopting BAC can reduce carbon consumption by 50% to 70%. Design standards and operational guidelines are being developed by American Water Works Association and International Water Association.

Opportunity 3: Indoor air quality and EV cabin filtration. Post pandemic awareness of airborne disease transmission and rising concerns about vehicle cabin air pollution have accelerated demand for high efficiency particulate air (HEPA) and activated carbon combination filters. Electric vehicles (EVs) with sealed cabins and recirculation modes rely on activated carbon filters to remove volatile organic compounds, nitrogen dioxide, and ozone. The global automotive cabin air filter market is forecast to grow at 9% CAGR to 2026, with coal based activated carbon preferred for its low cost and high gas phase adsorption capacity. Manufacturers should develop low pressure drop, high dust holding capacity formats tailored to HVAC systems.

Strategic recommendations:

- Invest in thermal reactivation facilities to capture aftermarket revenue and reduce customer total cost of ownership. Reactivated carbon can be sold at 50-60% of virgin carbon price while maintaining 85-95% performance.

- Diversify coal feedstock sources to mitigate supply disruptions and price volatility. Establish relationships with mines in Australia, Russia, South Africa, and Colombia.

- Form long term framework agreements (5-10 years) with large water utilities, gold mining companies, and power generators to secure stable demand and enable production planning.

- Develop digital tools for saturation monitoring and predictive carbon replacement, offering as a service model to differentiate from commodity suppliers.

- Monitor regulatory developments in PFAS, microplastics, and emerging contaminants to align R&D with upcoming compliance deadlines.

Conclusion and Summary

The coal based activated carbon market from 2024 to 2026 is characterized by robust growth driven by environmental regulations, water infrastructure investments, and industrial expansion. Manufacturers who embrace reactivation, pore size engineering, and smart monitoring will outperform commodity producers. Regional opportunities in Asia Pacific and Africa offer the highest growth rates, while PFAS remediation and electric vehicle filtration represent the most promising emerging applications. Industry stakeholders should prioritize technological innovation, supply chain resilience, and strategic partnerships to capture value in this evolving landscape.